Illinois, or the Prairie State as some call it, is home to 2.1 million small businesses, with over 232,000 located in the Windy City of Chicago, making it one of the most populous states for small businesses. During the COVID-19 pandemic, nearly 35% of the state’s small businesses were forced to shutter either temporarily or permanently, and rising interest rates, worker shortages and spiking inflation are further squeezing them.

Now is the time for small businesses in the state to search high and low for grant opportunities and contests in which they can gain access to free money in order to survive. Here is a list of grants and contests on both a national and local level that are still available to Illinois-based small businesses.

On a National Level:

Kapitus’ $250K Building Resilient Businesses Contest – Deadline is Looming!

Kapitus has launched its Building Resilient Businesses contest, in which one first-place winner will receive $100,000; one second-place winner will receive $50,000 and five third-place winners will each receive $20,000. To enter, simply send a homemade, 2-minute video briefly describing your business, how it was able to persevere over the last two years, and how you would spend $100,000. The contest is open to all small businesses in the US (excluding Vermont and Colorado) that have been in business for at least a year and have less than $5 million in annual revenue. The deadline to apply is June 30, 2022. To enter the contest, click here.

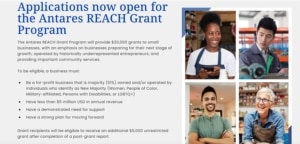

Antares REACH Grant Program

Small business consulting firm Hello Alice will award $20,000 in grants to women- and minority-owned

The Antares REACH Grant program is giving away $20,000 to women- and minority-owned small businesses nationwide.

businesses to help them prepare for the next stages of growth. The grants are being funded by Chicago-based private equity firm Antares Capital. Applicants must have less than $5 million in annual revenue, have a demonstrated need for support and a strong business plan for growth. Grant winners will be eligible for an additional $5,000 in funding after completion of a post-grant support. The deadline for applications is July 15, 2020. To apply, you are required to become a member of Hello Alice’s community of small businesses. For more information, click here.

WomensNet Amber Grant

WomensNet gives away one $10,000 grant and four $1000 grants to women-owned businesses in distinct categories every month such as skilled trades (January), hair care and beauty products (August) and Creative Arts (October). The site also gives grants of $25,000 to two businesses each at the end of each year, with both of them being previous $10,000 monthly grant winners. Applications are due on the last day of every month. To apply, click here.

American Express and Main Street America’s Inclusive Backing Grants

AmEx and Main Street America are providing more than 300 grants of $5,000 each over four cycles throughout 2022 to small businesses located in older or historic commercial districts with priority to be given to small businesses owned by the LGBTQ+ community, Hispanic-owned, veteran-owned, and business owners who are women and people of color. Applications for the fourth grant cycle are now being accepted by business owners who identify as native or indigenous people, Hispanic, LGBTQ+ and immigrants and refugees. Membership in the National Main Street Center is not required. Applications for the fourth grant cycle can be found here.

Skip Monthly Business Grant

Skip is a California-based social media company that helps both people and businesses get access to government-related services and information and is part of YoGov.org. Every month since March 2020, Skip uses revenues from its YouTube channel which awards $1,000 grants to small business owners as well as free services and information. The winner is announced on its YouTube channel on the third Wednesday of every month. For more information and to apply, click here.

State Level: Open to Illinois Small Businesses Only

The Land of Lincoln also has several grant and contest opportunities, especially in Chicago, that are still open:

Neighborhood Opportunity Fund Grants

Chicago’s Neighborhood Opportunity Fund is giving away grants three times in 2022 to small businesses in Chicago’s West, Southwest, and South sides to make improvements to their physical locations. These improvements can include land acquisition for expansion, roofing replacement or repairs and money to cover financing fees for a loan or lines of credit. The awards are up to $250,000 for small improvement projects and over $250,000 to $2.5 million for large projects. Deadlines for the second and third rounds of applications have not yet been established, but you can still apply. To learn more, click here.

City of Chicago’s Annual Business Plan Competition

The city of Chicago is giving away several grants to keep its small businesses afloat.

Chicago’s Office of the Treasurer Stephanie Neely is administering a contest to startups and young businesses in Chicago. The first-place winner, to be announced sometime in October, will take home $5,000. To enter, a small business must be a startup or no more than three-years-old with annual revenues of no more than $2 million. Applicants must submit their business plans as well as templates for their executive summaries. Applications are due on July 6, 2022. To learn more, click here.

Restaurant Employee Relief Fund

The Illinois Restaurant Association Education Relief Foundation is awarding grants to restaurant employees who have faced personal and financial hardships within the past 90 days to encourage food service workers in the state to remain at their jobs. Those hardships include unexpected illness or injury, death of a family member or a natural disaster. The grants range from $250 to $1,500. While not paid directly to business owners, this grant can help owners make things a little easier on staff that is sticking it out through the hard times. Deadline to apply is August 31, 2022. To apply, click here.

Small Business Improvement Fund (SBIF) Remodeling Grants

The SBIF Remodeling grants are aimed at larger small businesses in Chicago with physical locations that are seeking to remodel or visually improve their business locations. To be eligible, the applicant must employ up to 200 workers, and have an average of $9 million in annual sales over the previous three years. Or commercial property owners with a net worth of up to $9 million and liquid assets of up to $500,000. The grant will cover 30% to 90% of a business’ remodeling work up to $150,000. The first deadline for applications is June 30, 2022, while the second and third deadlines are on August 1st and August 31st, respectively. To learn more, click here.

Don’t Give Up Free Money!

With most federal pandemic aid programs dried up and current economic challenges such as inflation and rising interest rates putting a further squeeze on small businesses, it is more important than ever to apply for a chance to get free money for your business, be it through local or national grants or contests.

Related Articles:

Small Business Grants and Contests Still Available in New Jersey

Small Business Grants and Contests Still Available in Florida

Small Business Grants Still Available in California

Small Business Grants Still Available in New York

California has one of the largest Hispanic and LGBTQ populations in the country, so the American Express and Mainstreet America’s Inclusive Backing Grants national program very much so pertains to the Golden state. AmEx and Main Street America is providing more than 300 grants of $5,000 each over four cycles throughout 2022 to small businesses located in older or historic commercial districts with priority to be given to small businesses owned by the LBGTQ+ community, Hispanic-owned, veteran-owned, and business owners who are women and people of color. Applications for the fourth grant cycle are now being accepted by business owners who identify as native or indigenous people, Hispanic, LGBTQ+ and immigrants and refugees. Membership in the National Main Street Center is not required. Applications for the fourth grant cycle can be found

California has one of the largest Hispanic and LGBTQ populations in the country, so the American Express and Mainstreet America’s Inclusive Backing Grants national program very much so pertains to the Golden state. AmEx and Main Street America is providing more than 300 grants of $5,000 each over four cycles throughout 2022 to small businesses located in older or historic commercial districts with priority to be given to small businesses owned by the LBGTQ+ community, Hispanic-owned, veteran-owned, and business owners who are women and people of color. Applications for the fourth grant cycle are now being accepted by business owners who identify as native or indigenous people, Hispanic, LGBTQ+ and immigrants and refugees. Membership in the National Main Street Center is not required. Applications for the fourth grant cycle can be found